When it comes to growing your investments in mutual funds, a Dividend Reinvestment Plan (DRIP) is a popular strategy. Instead of receiving dividends as cash, you use those dividends to buy more units of the fund. This approach can compound your returns over time, helping your wealth grow steadily. However, it is crucial to understand how income tax slabs affect the tax you pay on dividends, which can influence the effectiveness of your reinvestment strategy. Knowing the interplay between dividend taxation and your income tax slab allows you to plan better and optimise your mutual fund investments.

In this article, we will explore the workings of Dividend Reinvestment Plans, how income tax slabs come into play, and what this means for your overall returns. We will break down the tax rules governing dividends and show how to make smarter choices by considering your tax bracket.

What is a dividend reinvestment plan

A Dividend Reinvestment Plan allows mutual fund investors to automatically use dividends to purchase additional units instead of receiving cash payouts. This means your investment grows without you having to make any fresh contributions. Over time, such compounding can potentially increase your corpus significantly.

Dividend reinvestment is a way to keep your money invested and working for you continuously. Instead of spending or withdrawing dividends, you reinvest them, thus making the power of compounding work efficiently. Many investors choose DRIPs to build wealth steadily over years without active intervention.

How are dividends taxed under indian income tax slabs

Although dividends from mutual funds are earnings, they attract taxation under Indian income tax laws. Since 2020, dividends are taxable in the hands of the investor at their applicable income tax slab rate, rather than being taxed at the fund level. This change has made it important for investors to know which tax bracket they fall under.

Here is what happens based on your income tax slabs:

– Individuals with income up to Rs. 2.5 lakh: No tax on dividend income.

– Income between Rs. 2.5 lakh and Rs. 5 lakh: Taxed at 5%.

– Income between Rs. 5 lakh and Rs. 10 lakh: Taxed at 20%.

– Income above Rs. 10 lakh: Taxed at 30%.

Dividends are added to your total income and taxed accordingly. Therefore, higher-income investors pay tax at higher rates on dividend income. It is essential to note that a TDS (Tax Deducted at Source) of 10% applies if dividend income exceeds Rs. 5,000 in a financial year.

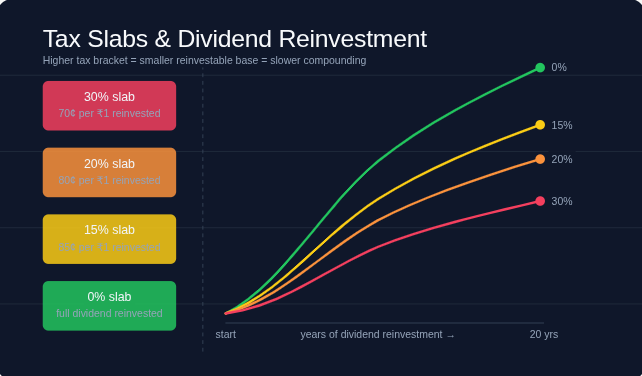

Impact of income tax slabs on dividend reinvestment plans

Understanding how your income tax slab influences dividend taxation is critical when using a Dividend Reinvestment Plan. Since dividends are taxable as per your slab rates, the returns from reinvested dividends are effectively lowered by the tax paid.

For example, suppose you receive Rs. 10,000 as dividends and are in the 30% slab. You owe Rs. 3,000 as tax, reducing the amount available to reinvest to Rs. 7,000. This lowers the compounding benefit that DRIPs seek to provide. On the other hand, if your income is below Rs. 2.5 lakh, you can reinvest the entire dividend without worrying about tax deductions, maximising growth.

Investors in higher tax brackets must consider the tax impact on reinvested dividends closely. Paying tax upfront on dividends reduces the capital that could have grown within the mutual fund. Therefore, evaluating whether to opt for dividend payout or reinvestment can make a real difference over time.

Tax implications when dividends are reinvested

With dividend reinvestment, the dividends are not received as cash but used to purchase more units. However, this does not exempt them from tax. Dividends remain taxable under your income tax slab, regardless of whether you take the cash or reinvest.

Another important point is the cost of acquisition of these additional units. When you reinvest dividends, the units bought have a purchase cost equal to the dividend amount. This cost becomes relevant when you redeem the units, as it affects the capital gains tax calculation.

Capital gains on redemption are classified based on the holding period:

– Short-term capital gains: Units held for less than three years are taxed at 15%.

– Long-term capital gains: Units held for more than three years have gains exceeding Rs. 1 lakh taxed at 10%.

The cost price adjustment because of reinvested dividends helps correctly compute these gains. This aspect makes DRIPs somewhat tax-efficient in the long run but requires record-keeping.

Strategies to optimise dividend reinvestment considering income tax slabs

- Choose growth funds instead of dividend funds: Growth funds do not pay dividends but instead reinvest returns internally. This avoids immediate tax liability on dividends, making them suitable for individuals in higher tax slabs.

- Use the Dividend Reinvestment Plan only if in lower tax brackets: If your income is below taxable limits or falls under 5%, DRIPs can enhance compounding significantly without much tax drag.

- Maintain detailed records: Keep track of units purchased through reinvested dividends to calculate cost of acquisition accurately and manage capital gains tax efficiently.

- Consider tax-saving mutual funds (ELSS): These offer deductions under Section 80C and help lower your taxable income, potentially keeping dividend tax lower due to reduced tax slabs.

- Plan withdrawals considering capital gains tax: Since capital gains have different taxation rules, timing your redemption to enjoy long-term capital gains benefits can enhance net returns.

Conclusion

Dividend Reinvestment Plans offer an effective way to grow your mutual fund investments by compounding your returns automatically. However, the impact of income tax slabs on dividend income is a critical factor that affects the amount available for reinvestment and ultimately your wealth accumulation. Dividends are taxable according to your income tax bracket, which means higher-income investors pay more tax, lowering the reinvested amount.

Keeping the relationship between income tax slabs and dividend tax in mind can help you make informed choices about opting for dividend reinvestment versus dividend payouts. Proper tax planning combined with informed investment strategy is the key to maximise the benefits of Dividend Reinvestment Plans. By understanding how income tax slabs impact dividend reinvestment, you can better align your mutual fund investments with your financial goals and tax situation.